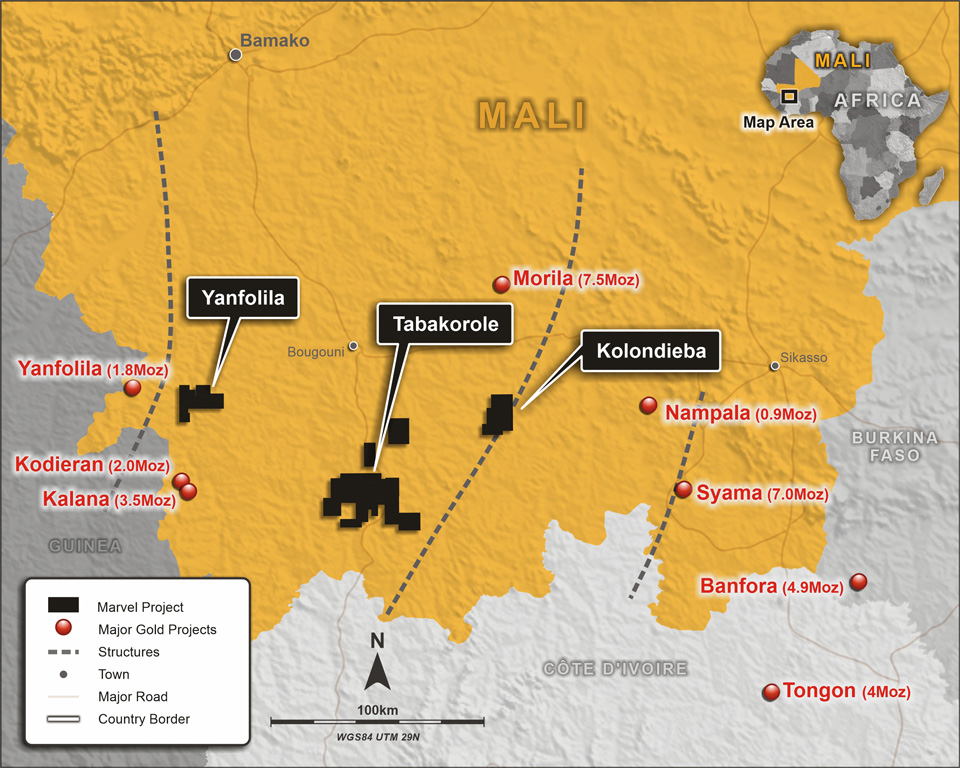

Projects

Marvel Project Portfolio

Since July 2020, Marvel has assembled a portfolio of advanced gold exploration projects in South Mali following acquisitions and joint ventures with ASX-listed Oklo Resources Limited and UK-listed Altus Strategies plc.